Helping VC and PE Funds Achieve Their Goals

For Venture Capital funds, an external partner adds immediate value by extending the fund’s platform, diligence, and portfolio-support capacity without increasing permanent headcount. Such a partner can help identify stronger startups, assess technical and commercial risks, validate markets, support founders with pilots and customer access, prepare companies for the next funding round, and accelerate international growth. This improves the VC’s ability to win competitive deals, support portfolio companies after investment, increase follow-on value, and create better conditions for IPO, M&A, or secondary exits.

For Private Equity funds, an external partner helps convert the investment thesis into measurable operational value. By supporting due diligence, 100-day plans, digital transformation, KPI systems, pricing, procurement, AI adoption, ESG readiness, add-on strategy, and exit preparation, the partner helps the PE fund increase EBITDA, reduce execution risk, professionalize portfolio companies, and improve the timing and quality of exits. This directly supports the PE fund’s core objectives: stronger cashflows, faster value creation, higher MOIC, better IRR, and more credible reporting to LPs.

Dilutive Funding Ecosystem

How Venture Capital Is Structured

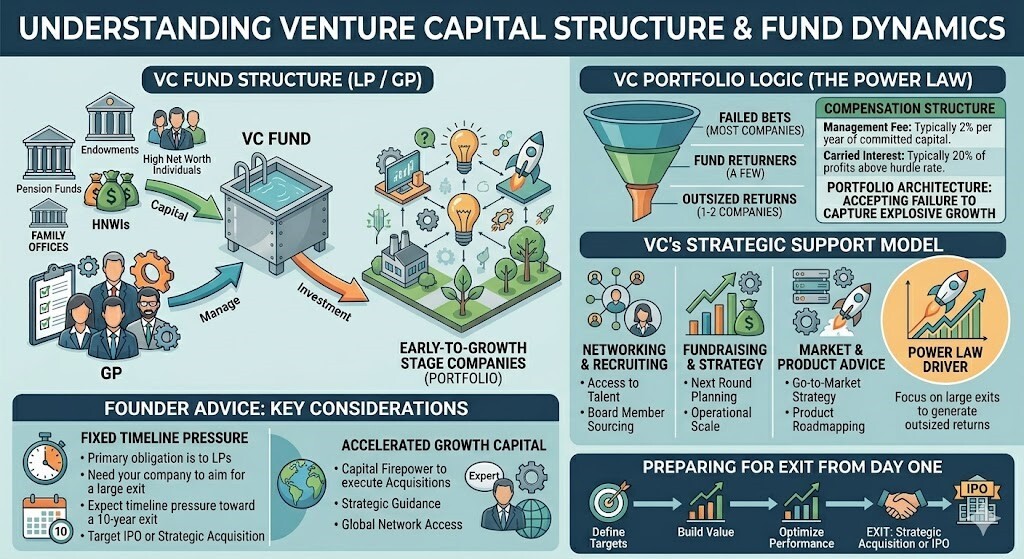

A venture capital firm raises a closed-end fund from institutional investors — pension funds, endowments, family offices, and high-net-worth individuals — who become Limited Partners (LPs) and commit capital for a fixed period, typically ten years. The firm's partners, the General Partners (GPs), manage that capital, source deals, and make investment decisions in exchange for a management fee (usually 2% of committed capital per year) and carried interest (typically 20% of profits above a hurdle rate). The GP deploys capital across a portfolio of early-to-growth stage companies, accepting that most bets will fail, a few will return the fund, and one or two will generate the outsized returns that define the fund's performance. This portfolio logic is not incidental — it is the architecture of the model. For founders, understanding this means understanding that a VC's primary obligation is to their LPs, that they need your company to aim for a large exit, and that their timeline is fixed: expect pressure toward an IPO or acquisition well within the fund's life.

How Private Equity Is Structured

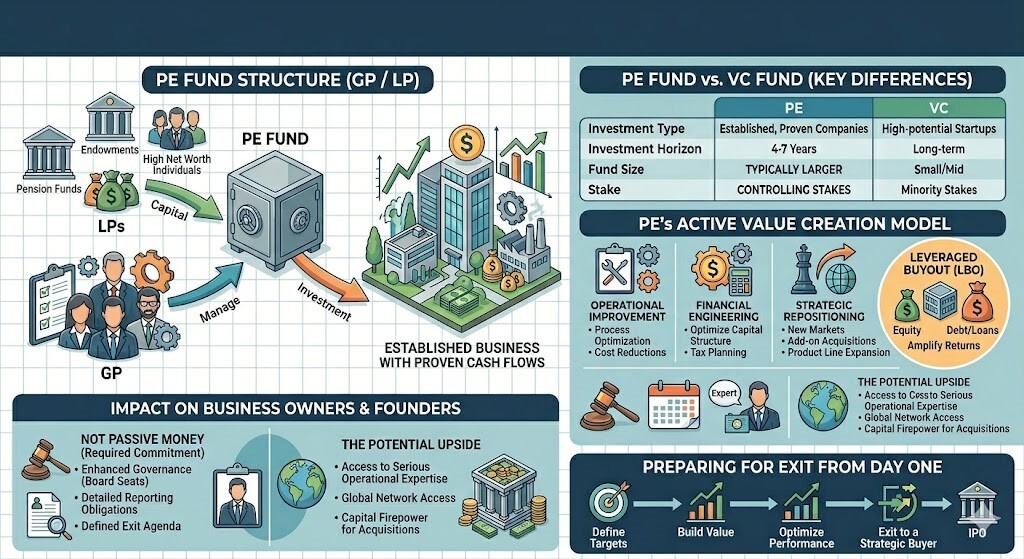

Private equity operates on a similar fund structure — GP manages capital raised from LPs — but the resemblance to venture capital stops there. PE funds are typically larger, the investment horizon is shorter (four to seven years), and the model relies heavily on acquiring controlling stakes in established businesses with proven cash flows. Rather than betting on potential, PE creates value through operational improvement, financial engineering, and strategic repositioning — often using leverage (borrowed capital) to amplify returns, a strategy known as a leveraged buyout (LBO). Within a PE-backed company, the fund installs or works closely with management, sets clear performance targets, and actively prepares the business for exit from day one. For founders and business owners, this means PE is not passive money — it comes with governance, reporting obligations, and a defined exit agenda. The upside is access to serious operational expertise, a global network, and the capital firepower to execute acquisitions that would be impossible to fund organically.